Every borrower is screened. Twice.

250+ data points assessed by BQS™. Credit, income, behaviour, intent. Only the best make it through.

Explainer: How P2P lending works.

A credit score tells you where a borrower has been. BQS™tells you where they are headed — across 5 pillars and 250+ data points, every single time.

A credit score tells you where a borrower has been. BQS™tells you where they are headed — across 5 pillars and 250+ data points, every single time.

Identity and compliance

Credit history

Income and cash flow

Repayment capacity

Stability and behaviour

10/10

Don’t just pay EMIs, earn them via 1 Finance P2P Lending.

This is what your money earns through us.

Living in India

Living in India At least 18 years old

At least 18 years old Indian bank account

Indian bank account250+ data points assessed by BQS™. Credit, income, behaviour, intent. Only the best make it through.

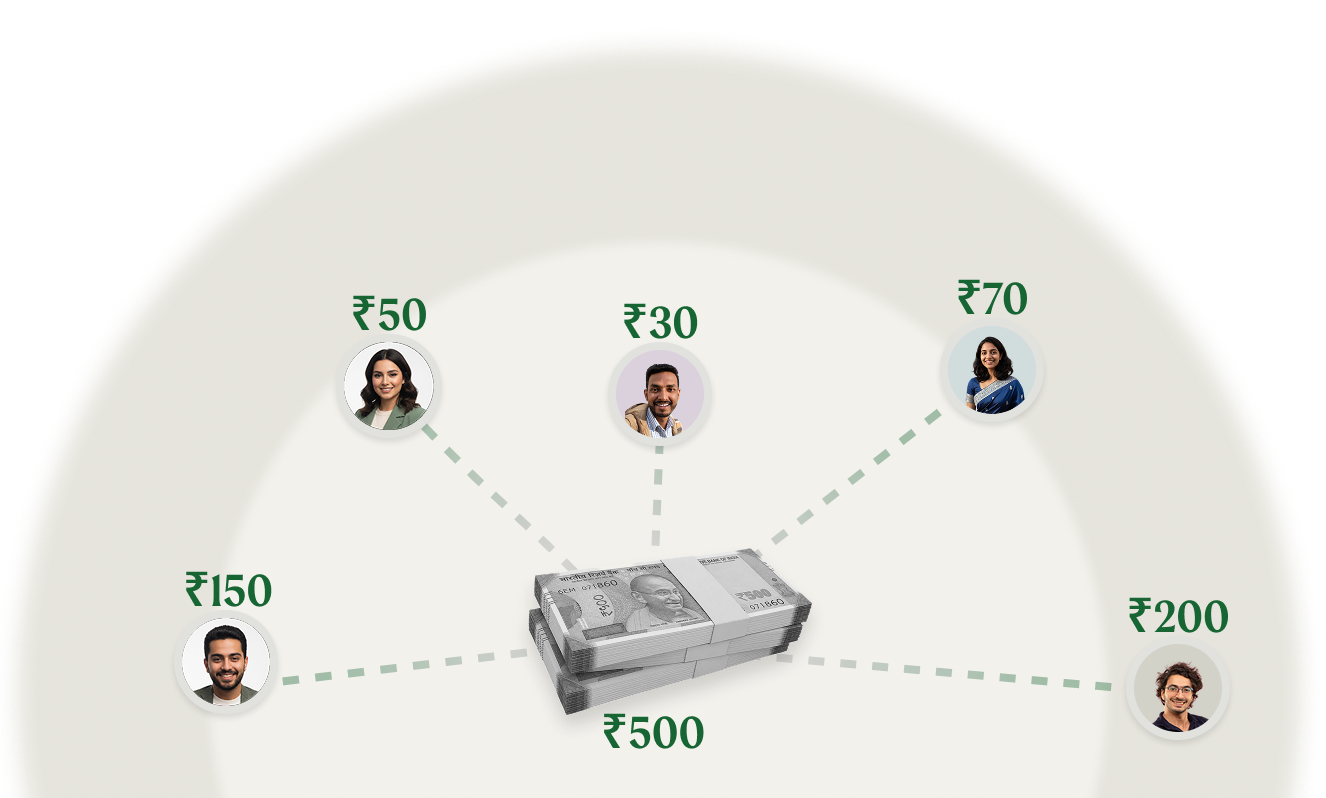

Your money comes back every month with interest. Re-lend it. Let compounding do the rest.

Equity and gold may fluctuate. Diversified lending helps reduce risk across multiple borrowers and support steadier monthly cash flows.

Diversified borrower exposure helps create regular monthly cash flows, with risks kept transparent.

Every rupee you lend is distributed across multiple screened borrowers. We cap your exposure to any single borrower at 5% which means your money is never concentrated in one place. Your portfolio stays balanced. Your portfolio stays balanced, and no single default can derail it.

Want to understand risk diversification better?

14.8%

Annual industry growth rate. India's fastest growing asset classes.

27+

RBI-registered NBFC-P2P platforms officially recognised and overseen by RBI since 2017.

$38.18B

Projected market size by 2031

Here’s a list of a few common questions that might help. If you have any other questions, you can email or text us on WhatsApp.

Peer-to-peer (P2P) lending connects borrowers and lenders directly. It allows borrowers to get loans quickly and lets lenders earn money on their returns. This is all done through a safe and regulated online platform. Lenders can choose whom to lend to, helping them diversify their portfolios.

Yes, P2P lending is regulated by the Reserve Bank of India (RBI). Since P2P platforms engage in lending and borrowing, the RBI mandates that they be registered as P2P non-banking financial companies (NBFCs).

1 Finance P2P is a Reserve Bank of India (RBI) registered NBFC-P2P with a simple vision: to make credit more accessible and lending more rewarding. We select high-quality borrowers, and lenders can earn up to 16% p.a. depending on borrower repayment. For borrowers, we provide loans at the best rates in the industry.

Yes, 1 Finance P2P is officially registered as an NBFC-P2P with the RBI. It ensures we offer a safe and regulated platform for peer-to-peer lending and borrowing throughout India.

Anyone who is a resident of India, has an Indian bank account, and is at least 18 years old can become a lender at 1 Finance P2P.

1 Finance P2P helps you diversify beyond traditional asset classes by lending directly to individually assessed borrowers. Every borrower is evaluated through our proprietary Borrower Quality Score™ (BQS), which assesses more than 250 data points across income stability, cash flow, repayment capacity and credit behaviour — and only around 3% of applicants make it through. Diversification further reduces your risk: no more than 5% of your total lending is allocated to any single borrower. As borrowers repay their EMIs, you earn interest income every month, with returns of up to 16% p.a. possible depending on borrower repayment. Please note: P2P lending carries risk. Borrowers may default, and your principal is not guaranteed or insured by the platform or the RBI.

If a borrower defaults, P2P lending platforms take steps to recover the loan, such as sending reminders, charging late fees, and reporting to credit bureaus. In severe cases, legal action may be taken; however, the lender ultimately incurs the financial loss.

At 1 Finance P2P, we help manage risk your money by diversifying your funds across multiple borrowers. No more than 5% of your capital is ever lent to a single borrower, minimising risk. Additionally, we have a stringent credit underwriting process that evaluates over 250 parameters before approving loans. It ensures you lend only to high-quality, creditworthy borrowers, reducing your risk of default.

To borrow from 1 Finance P2P, you need to be at least 18 years old and not more than 60 years of age, and hold a valid bank account. KYC documents are also required to apply for a loan on P2P lending platforms. The total borrowing limit across all platforms is capped at ₹10 lakh at any given time.

You can apply for a maximum online loan of up to ₹10 lakh from 1 Finance P2P. The minimum amount you can borrow is ₹10,000. Remember that you can apply for a loan up to ₹10 lakh across all P2P lending platforms at any point in time.

Borrowers will be charged an interest rate based on their risk profile. The interest rate will range from 8% to 24%.

A borrower can avail a loan for up to 36 months. The actual tenure depends on the loan amount and the credit profile. However, as per RBI guidelines, the maximum tenure for a P2P loan cannot exceed 36 months.

At 1 Finance P2P, we believe in 100% transparency. While there is a nominal processing fee for borrowers to cover administrative and credit assessment costs, there are no hidden charges. All fees, interest rates, and repayment terms are clearly disclosed upfront before you finalise your loan or return, ensuring you stay in complete control of your finances.

email us

care@1financep2p.comFor a quick response to all your queries, reach out to us on WhatsApp.